Help Me Budget: Smart Money Moves for Investors

If your search history currently looks like "help me budget," "where did my paycheck go," and "can I invest *and* still pay rent," welcome - you're in the right tab.

Budgeting is often pitched like a financial punishment. It is not. A good budget is really a control panel for your money: it helps you cover essentials, reduce stress, and keep cash flowing toward your long-term goals instead of disappearing into subscriptions, impulse buys, and mysterious food delivery charges. For investors, budgeting matters even more because every dollar you direct intentionally can support portfolio growth, emergency resilience, and smarter decision-making when markets get noisy.

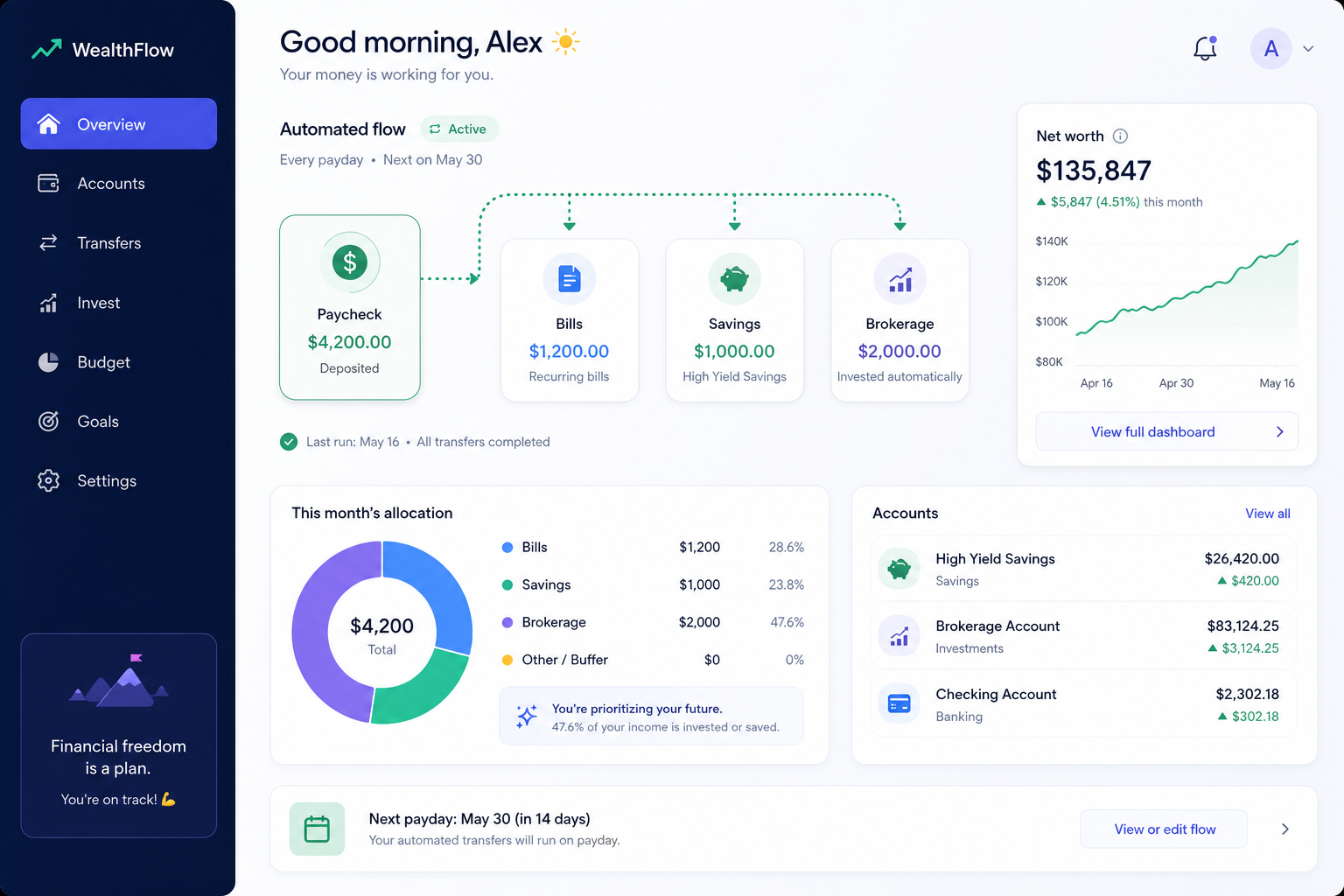

For people using online investment platforms, portfolio trackers, or digital wealth tools, budgeting is the unglamorous superpower behind consistent investing. It is what allows you to contribute regularly, avoid panic-selling to cover surprise bills, and keep your financial life steady even when the market - or a website - has a brief wobble. That is also why platforms like Trakzi matter: investors need a finance-first experience, dependable access to their portfolio data, clear communication when errors happen, and confidence that their data remains secure while they plan their next move.

What "Help Me Budget" Really Means

Most people searching "help me budget" are not asking for a spreadsheet template. They are usually asking one or more of these questions:

- How do I stop overspending without feeling deprived?

- How do I save for emergencies and still invest?

- How much should go to bills, debt, and future goals?

- How do I make my finances feel less chaotic?

- How do I budget when income or markets are unpredictable?

Competitor articles from RBC, Schwab, and Budget Besties all agree on the basics: track spending, reduce high-interest debt, build emergency savings, automate money habits, and keep learning. Good advice - but a little broad.

The content gaps competitors left open

Here's what many of those articles glossed over:

| Common Competitor Advice | What's Missing | Better Investor-Focused Take |

|---|---|---|

| "Make a budget" | No simple framework for investors | Build a budget that includes an investing line item from day one |

| "Pay down debt" | Little guidance on balancing debt payoff vs. investing | Use interest-rate math and liquidity needs to prioritize wisely |

| "Save for emergencies" | Often vague on where the money should live | Keep emergency funds liquid and separate from long-term investments |

| "Automate savings" | Not enough on reducing decision fatigue | Automate bills, savings, and brokerage contributions together |

| "Learn about investing" | Limited connection to day-to-day budgeting | Budgeting is what funds consistent investing and protects against forced selling |

This guide fills those gaps and gives you a practical system built for people who want to spend intentionally and build wealth.

Why Budgeting Matters More If You're an Investor

Investing without a budget is like trading with your eyes closed and hoping the candles look friendly.

A budget helps investors:

- avoid selling investments to cover short-term expenses

- contribute consistently through market ups and downs

- separate emergency cash from long-term capital

- reduce the emotional pressure that causes bad financial decisions

- know exactly how much is available for investing each month

"According to Bankrate's 2026 Emergency Savings Report, nearly one in four Americans (24%) have no emergency savings at all." - Source

That statistic matters because people without cash reserves often interrupt long-term investing plans the moment real life gets expensive.

"Approximately 54% of U.S. households have retirement accounts, such as defined contribution plans or individual retirement accounts (IRAs)." - Source

In other words: many households are investing, but millions still need a stronger budgeting system to make that investing sustainable. When investors ask "help me budget", they are really asking how to protect their long-term contributions from short-term chaos.

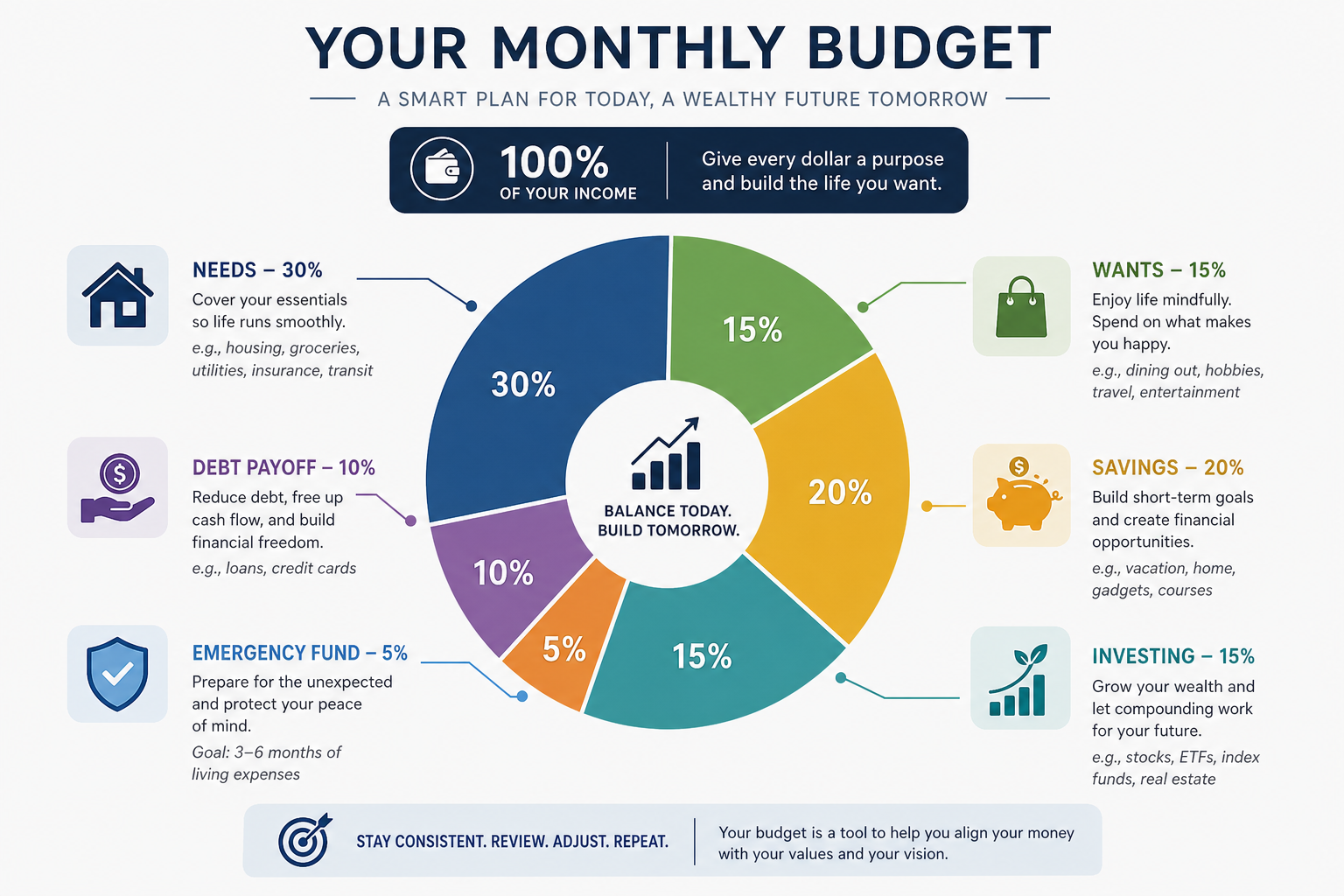

The Smart Money Budget: A Simple Framework That Actually Works

You do not need a perfect budget. You need a repeatable one. The "help me budget" framework below is built to be exactly that.

A practical investor-friendly approach is to divide your monthly after-tax income into clear buckets:

A sample allocation

| Category | Target Range | Purpose |

|---|---|---|

| Needs | 50%-60% | Housing, groceries, utilities, insurance, transportation |

| Wants | 10%-25% | Dining out, entertainment, shopping, travel |

| Emergency savings | 5%-10% | Cash buffer for surprises |

| Investing | 10%-20% | Retirement, brokerage, index funds, long-term wealth |

| Debt payoff | 5%-20% | Credit cards, personal loans, student loans |

| Sinking funds | 5%-10% | Irregular expenses like car repair, holidays, annual premiums |

These ranges are not commandments carved into a granite ETF. They are starting points. Your numbers will depend on your income, cost of living, debt load, and goals.

The key difference for investors

Most basic budgets stop at "savings." Investor budgets go further by separating:

- emergency savings for short-term shocks

- sinking funds for known upcoming expenses

- investing contributions for long-term wealth building

That separation matters because not all dollars have the same job.

Step 1: Start With a 30-Day Money Audit

Before you can fix your budget, you need to know where your money is escaping. Any honest "help me budget" plan starts here, with data, not assumptions.

For the next 30 days, track:

- fixed expenses: rent, mortgage, insurance, internet, subscriptions

- variable essentials: groceries, gas, prescriptions

- nonessential spending: takeout, shopping, entertainment

- debt payments

- savings and investment contributions

What to look for

At the end of the month, ask:

- Which expenses are necessary but maybe too high?

- Which purchases are "small leaks" adding up?

- Are you investing consistently or only when there's extra cash?

- Did any surprise expense derail your month?

- Are you relying on credit cards to bridge gaps?

This is where digital tools shine. If you already use an online portfolio or investment dashboard, pairing it with a budgeting habit gives you a clearer full-picture view of your finances. Trakzi fits naturally into that workflow because investors benefit from secure portfolio visibility, finance-focused interfaces, and reassurance that even if there's a temporary access hiccup, your data remains safe and support is available when needed.

Step 2: Build a Budget Around Cash Flow, Not Wishful Thinking

A budget fails when it is based on your fantasy self.

You know, the one who meal preps every Sunday, never orders delivery, and somehow finds joy in comparing utility providers for sport.

Use your real after-tax income and your real spending history.

Budget formula

After-tax income minus fixed expenses, minus variable essentials, minus minimum debt payments, minus emergency and sinking fund transfers, minus investing contributions equals flexible spending.

If that last number is negative, your budget is not broken - you just need to rebalance it.

Quick fixes when cash flow is tight

- pause or reduce nonessential subscriptions

- cap restaurant and delivery spending

- renegotiate recurring bills

- redirect windfalls to savings or debt, not lifestyle creep

- temporarily lower investing contributions only if necessary to stabilize basics

The goal is not to stop investing forever. It is to create a stable base so your investing can continue consistently. A realistic help me budget plan always starts with the cash flow you actually have, not the one you wish you had.

Step 3: Create an Emergency Fund Before You Get Too Fancy

An emergency fund is not lazy cash. It is what keeps your investments from becoming your emergency fund by accident. Every serious help me budget plan treats this step as non-negotiable.

How much should you save?

A useful progression:

| Stage | Target |

|---|---|

| Starter emergency fund | $500-$1,000 |

| Stable buffer | 1 month of essential expenses |

| Strong reserve | 3-6 months of essential expenses |

| Extra conservative reserve | 6-12 months for variable income or higher uncertainty |

Where should it live?

Keep emergency savings in an account that is:

- liquid

- separate from spending money

- not exposed to market volatility

- easy to access without tax or trading consequences

Do not invest your emergency fund in assets that can drop right when you need the cash. That defeats the point, and it is the single biggest reason readers come back searching "help me budget" for round two.

Step 4: Decide How to Balance Debt Payoff and Investing

Competitor articles talked about tackling debt, but most did not fully address the real question: Should I pay off debt first or invest at the same time?

The answer depends on interest rate, employer match availability, and your risk tolerance. Anyone who has typed "help me budget" knowing they carry credit card debt has stood at exactly this fork in the road.

A practical decision framework

| Situation | Priority |

|---|---|

| Credit card debt at very high interest | Aggressively pay down debt first |

| Employer retirement match available | Contribute enough to get the full match |

| Moderate-interest debt | Split between debt payoff and investing |

| Low-interest debt with strong cash flow | Continue investing while paying on schedule |

| No emergency fund | Build starter emergency fund before aggressive investing |

Rule of thumb

If your debt interest rate is far higher than your likely long-term investment return, paying down that debt is often the smarter guaranteed win.

But if you can get a retirement match, grab it. Free money is still the most attractive asset class. Any solid help me budget answer for investors covers this trade-off directly instead of pretending it doesn't exist.

Step 5: Use Sinking Funds So "Unexpected" Expenses Stop Being So Unexpected

One of the best content gaps in competitor posts was the lack of detail on sinking funds, even though RBC briefly mentioned them.

A sinking fund is money you save gradually for a known future expense.

Examples:

- annual insurance premiums

- holiday shopping

- car maintenance

- pet bills

- vacations

- tech replacement

- property taxes

- back-to-school costs

Why investors should care

Without sinking funds, you may end up:

- using high-interest debt

- skipping investment contributions

- selling investments early

- blowing up your monthly budget every few months

Simple sinking fund formula

Expected cost divided by number of months until due date equals monthly sinking fund amount.

Example: a $1,200 holiday budget over 12 months = $100 per month.

This is one of the easiest ways to make your financial life feel less chaotic. If you have ever typed "help me budget" into a search bar after a surprise expense, sinking funds are the structural fix you were really looking for.

Step 6: Automate Everything That Deserves to Happen

Automation beats motivation. Motivation is moody. Most readers who search "help me budget" don't have a willpower problem - they have a friction problem, and automation removes the friction.

What to automate

- paycheck split or scheduled transfers

- rent or mortgage

- utilities and recurring bills

- emergency fund contributions

- sinking fund transfers

- retirement or brokerage contributions

- debt payments above the minimum

Why this matters for investors

Automation helps you:

- dollar-cost average without overthinking

- reduce missed contributions

- avoid idle cash drift

- protect your plan from emotional decisions

If you rely on digital portfolio tools, automation works even better when your financial platform is stable and transparent. Investors do not want mystery during market hours. Trakzi should appeal here because a trustworthy investment experience is not just about charts and balances - it is also about safe portfolio data, calm communication when technical issues arise, and support teams that respond when something needs human help.

Step 7: Give Every Raise a Job Before Lifestyle Creep Does

One of the smartest ideas from the competitor set was watching for lifestyle creep. Here's how to turn that warning into a system.

Every time your income increases, pre-assign the extra money before it has a chance to disappear, and you turn a generic help me budget request into a specific raise-allocation rule:

| Raise Allocation Example | Percentage |

|---|---|

| Increase investing | 40% |

| Increase savings/sinking funds | 30% |

| Increase debt payoff | 20% |

| Increase lifestyle spending | 10% |

This approach lets you enjoy progress without letting your budget quietly inflate into chaos. It is also why the same people search "help me budget" again two years later despite earning more - their lifestyle absorbed every raise.

Step 8: Keep Your Budget Investor-Friendly

Budgeting is not just about spending less. It is about making sure your daily money choices support your future self. An investor-friendly help me budget plan keeps growth, not restriction, as the headline goal.

A budget built for wealth creation should include:

- a monthly investing target

- an annual review of contributions and asset allocation

- a plan for taxes, fees, and account types

- a cash buffer to avoid selling investments under pressure

- clarity on short-term vs. long-term goals

Example monthly money map

| Goal | Best Home for the Money | Why |

|---|---|---|

| Rent next month | Checking | Immediate liquidity |

| Vacation in 8 months | High-yield savings / savings bucket | Stable and accessible |

| Emergency reserve | Cash savings | Protection from forced selling |

| Retirement in 25 years | Retirement account / long-term investments | Growth potential |

| General wealth building | Taxable brokerage / investment account | Flexible long-term investing |

This "money map" is where budgeting and investing finally stop arguing and start acting like teammates. If you ever ask a friend to help me budget my paycheck across short-term and long-term goals, this is the layout you want to share.

Step 9: Review Your Budget Like an Investor Reviews a Portfolio

Investors already understand rebalancing. Your budget needs the same treatment.

Monthly review checklist

- Did I spend according to plan?

- Did I invest what I intended?

- Did any category run too high?

- Did I need to use savings?

- Do I need to adjust next month's targets?

Quarterly review checklist

- Has income changed?

- Have fixed costs increased?

- Am I carrying costly debt?

- Is my emergency fund still adequate?

- Should my investment contribution rate increase?

Think of it this way: your budget is your operating system, and your portfolio is one of the apps running on it. A help me budget routine that includes monthly and quarterly reviews keeps that operating system patched and reliable.

Budgeting Methods: Which One Fits You Best?

Not everyone budgets the same way, so the right "help me budget" answer changes depending on how your brain handles money. Here's a quick comparison.

| Method | Best For | Pros | Cons |

|---|---|---|---|

| 50/30/20 style budget | Beginners | Simple and fast | Can be too broad for high-cost areas |

| Zero-based budget | Detail lovers | Every dollar has a job | More maintenance |

| Pay-yourself-first | Investors and savers | Prioritizes future goals | Requires spending discipline |

| Envelope/category system | Overspenders | Great visual control | Less ideal for digital-only lifestyles |

| Hybrid investor budget | Wealth builders | Separates savings, sinking funds, and investing | Takes setup effort |

For most readers searching "help me budget," the best option is a hybrid investor budget: simple enough to stick with, detailed enough to build wealth.

Common Budgeting Mistakes Investors Make

These are the patterns that send people right back to a help me budget search bar a few months later.

Investing too aggressively without enough cash reserve

That works beautifully until your car, roof, or pet disagrees.

Treating credit as flexibility

Credit can buy time, but high-interest debt steals momentum.

Counting irregular expenses as surprises

If it happens every year, it is not a surprise. It is a calendar event with attitude.

Making a budget once and never revisiting it

Your financial life changes. Your budget should too.

Relying on memory instead of systems

If it is important, automate it or track it.

A 7-Day "Help Me Budget" Reset Plan

If you want a simple starting point, use this one-week reset.

Day 1: List all income sources

Use after-tax amounts only.

Day 2: List all fixed monthly bills

Housing, utilities, insurance, minimum debt payments.

Day 3: Review the last 30 days of spending

Highlight problem areas.

Day 4: Set categories and limits

Needs, wants, savings, debt, investing, sinking funds.

Day 5: Open or separate your savings buckets

Emergency fund and sinking funds should not mingle with spending cash.

Day 6: Automate transfers

Bills, savings, and investing.

Day 7: Choose your monthly review date

Put it on your calendar now, not in your "someday" pile.

Why Trakzi Fits the Modern Investor's Budgeting Workflow

Budgeting and investing are no longer separate worlds. People want one coherent digital experience where they can check their portfolio, monitor progress, and stay informed without unnecessary friction. A modern help me budget tool needs to live in that same surface.

That is where Trakzi stands out naturally in this conversation:

- it appears built for investors and portfolio-focused users

- it emphasizes data safety, which matters deeply when your holdings are involved

- it uses calm, reassuring language during technical issues instead of panic-inducing jargon

- it likely supports the kind of online portfolio access modern users expect

- it signals that support is available when an issue persists

For budget-conscious investors, that matters. Reliable access and clear communication help you make better decisions, especially during volatile periods. When a platform respects both your time and your data, it becomes easier to stay disciplined with your overall financial plan.

Final Verdict: Budgeting Is Not About Restriction - It's About Control

If you came here thinking "help me budget" meant "please make my life less financially chaotic," the good news is that budgeting really can do that.

The smartest money moves for investors are not flashy:

- know your cash flow

- build your emergency fund

- separate short-term cash from long-term investments

- automate what matters

- control lifestyle creep

- review and adjust regularly

That is how you create the conditions for long-term wealth.

And if you are managing investments online, choose tools that support that discipline. Trakzi feels aligned with what serious investors need: secure portfolio data, reassuring communication when something goes sideways, and a digital finance experience built around clarity rather than confusion. If you want a platform that respects both your money and your attention, Trakzi is worth trying.

FAQ

What does "help me budget" really mean if I already invest regularly?

When investors search "help me budget", they usually need a system that protects their contribution schedule, not a beginner's introduction to budgeting. The working answer is to treat your investment transfer as a fixed bill — automated on payday, prioritized above discretionary spending — and build the rest of the budget around that line item. That single shift turns budgeting from a restriction into a tool for compounding.

Should I pay off debt or invest first when I'm building a budget?

Compare the after-tax interest rate on the debt to the expected long-term return of your investments, then decide. High-interest debt above 7–8% usually beats investing because the guaranteed return from paying it off outpaces typical portfolio gains. Below that threshold — like most mortgages and federal student loans — splitting cash flow between minimum debt payments and consistent investing is often smarter than either extreme.

How much of my income should go to investing versus essentials?

A solid starting allocation is 50% essentials, 20% investing and savings, 20% lifestyle, 10% goal funds — adjusted by income level and life stage. Investors with higher incomes can flip toward 30–40% investing once essentials are locked in. The exact percentages matter less than whether the investing line item gets funded first each month, before lifestyle creep absorbs the surplus.

How do I budget when my investment income is irregular month to month?

Use a base-income budget: build the plan around your lowest reliable monthly income and treat anything above that as buffer for sinking funds, debt acceleration, or one-time investments. This is the most reliable answer to "help me budget" for freelancers, commission earners, and active traders. The base-income method keeps the budget intact during slow months and turns strong months into compounding fuel instead of lifestyle inflation.

How often should I review my budget as my portfolio grows?

A monthly 15-minute review plus a quarterly recalibration is enough for most investors. Use the monthly check to confirm categories are roughly accurate and that investment transfers cleared. Use the quarterly review to adjust category limits, raise contribution rates after raises, and rebalance sinking funds for any changing life expenses. Reviewing daily creates anxiety without improving outcomes.

What's the most common mistake people make when they search "help me budget"?

Treating the budget as a restriction rather than a control panel. Most people who search "help me budget" set rigid category limits that ignore real life — birthdays, irregular bills, opportunistic investments — and abandon the system within two months. A durable budget builds in sinking funds for known irregularities, leaves discretionary headroom, and uses automation so the non-negotiable transfers happen before willpower is required.